‘E-Invoicing’ or ‘Electronic Invoicing’ is a system in which B2B invoices and a few other documents are authenticated electronically by GSTN for further use on the common GST portal.

Who is Required to Generate e-invoice?

As per the new rules of GST on e-invoicing, all businesses having a turnover exceeding Rs.5 crore have to generate e-invoice. This threshold was Rs.10 crore before the latest amendment.

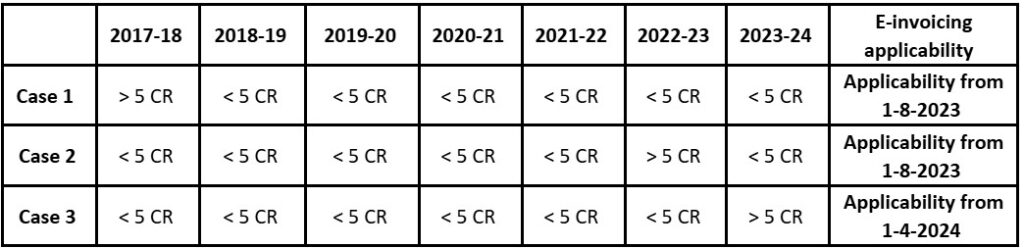

How to calculate E-Invoicing applicability for business having turnover more than 5 crores?

How E – invoicing is generated?

Taxpayer first prepares and generates his invoice using his own billing system or manual system.

Details of the invoice are uploaded or reported by the taxpayer to invoice registration IRP. This way the taxpayer registers his supply transaction on IRP. On uploading IRP returns E-invoice with a unique “Invoice Reference Number” [IRN] after digitally signing E-invoice and adding QR code

To which transactions and documents does e-Invoicing apply to?

Documents:

Tax invoices, credit notes and debit notes under Section 34 of the CGST Act

Transactions:

Taxable Business-to-Business sale of goods or services, Business-to-government sale of goods or services, exports, deemed exports, supplies to SEZ (with or without tax payment), stock transfers or supply of services to distinct persons, SEZ developers, and supplies under reverse charge covered by Section 9(3) of the CGST Act.

Exemption from E - invoicing?

1)A banking company or a financial institution, including an NBFC

2) A Goods Transport Agency (GTA)

3) A registered person supplying passenger transportation services

4) A registered person supplying services by way of admission to the exhibition of cinematographic films in multiplex services

5) A government department and Local authority

6) An SEZ unit (Special Economic Zone) (excluded via CBIC Notification No. 61/2020 – Central Tax)

7) Persons registered in terms of Rule 14 of CGST Rules (OIDAR)

8) B2C invoices are also exempted from e-invoicing.

9) Supplies Received from unregistered person.

What happens if I don't generate an e invoice?

Non-generation of e-invoices will imply non-intimation of supply transactions to the government. Any invoice issued by the applicable taxpayer without the IRN is considered an invalid invoice under GST law.

If your AATO has crossed the e-invoicing turnover limit and you’re exempt from e-invoicing as per the mandate, then you need to mention the following declaration on the invoice:

“I/We hereby declare that though our aggregate turnover in any preceding financial year from 2017-18 onwards is more than the aggregate turnover notified under sub-rule (4) of rule 48, we are not required to prepare an invoice in terms of the provisions of the said sub-rule.”