The Composition Scheme is a simplified tax scheme under GST for small taxpayers, allowing them to pay tax at a reduced rate based on turnover, instead of the regular tax rates. It is available for manufacturers, dealers, and certain service providers, with fewer compliance requirements.

Who Can Opt for Composition Scheme?

Manufacturers of Goods

Traders

Restaurants (excluding those serving alcohol)

Who Cannot Opt for Composition Scheme?

Manufacturers of items like ice cream, pan masala, or tobacco

Businesses engaged in interstate supplies

Casual taxable persons, non-resident taxable persons, and others involved in non-taxable supplies

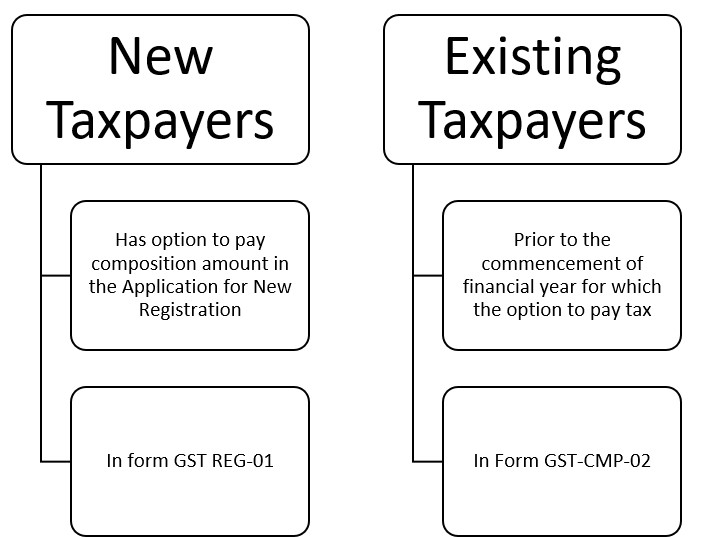

When can I Opt for Composition Scheme ?

Understanding Eligibility for the GST Composition Scheme

Businesses with an annual aggregate turnover up to Rs.1.5 crore (75 lakhs for special category states) can opt into the composition scheme.

*Special category State: Arunachal Pradesh, Assam, Jammu and Kashmir, Manipur, Meghalaya, Mizoram, Nagaland, Sikkim, Tripura, Himachal Pradesh and Uttarakhand.

Only manufacturers of goods, dealers, and restaurants (not serving alcohol) can opt for the composition scheme under Section 10. However, service providers can opt into a similar scheme for composition dealers notified by the CGST (Rate) notification no. 2/2019 dated 7th March 2019 where the total turnover limit is Rs.50 lakh.

Further, the government introduced a separate composition scheme on 31st March 2022 for the manufacturers of bricks, including building bricks, bricks of fossil meals or similar siliceous earths, earthen or roofing tiles, and fly ash bricks and blocks. Those who have opted in can pay a special rate of tax at 6%, without input tax credit.

Example 1 for Eligibility: If a business’s aggregate turnover in the previous financial year was Rs. 1.2 crore, it would qualify for the composition scheme.

Example 2 for Eligibility: If a business had an aggregate turnover of Rs. 1.2 crore in the previous financial year and makes interstate supplies, it would not qualify for the Composition Scheme.

Aggregate turnover

The aggregate turnover is computed on an all-India basis for the person having the same PAN. It includes taxable supplies, exempt supplies, exports, and inter-state supplies.

Composition scheme : Applicable GST Rate

Type of Business

CGST

SGST

Total

Manufacturers and Traders (Goods

0.5%

0.5%

1%

Restaurants not serving Alcohol

2.5%

2.5%

5%

Service Providers

3%

3%

6%

Manufacturers of bricks (including building bricks, bricks of fossil meals or similar siliceous earths, earthen or roofing tiles, and fly ash bricks and blocks )

3%

3%

6%

Treatment for input credit availed when transitioning from normal scheme to composition scheme

When switching from normal scheme to composition scheme, the taxpayer shall be liable to pay an amount equal to the credit of input tax in respect of inputs held in stock on the day immediately preceding the date of such switchover. The balance of input tax credit after payment of such amount, if any, lying in the credit ledger shall lapse.

Conditions for availing input credit on stock lying at the time of transition

Following are the conditions which must be addressed by the taxpayer to avail credit on input at the time of transition from composition scheme to the normal scheme:

Inputs or goods will be used for making taxable supplies.

The CENVAT Credit was eligible to be claimed in the previous regime. However, one couldn’t claim it under the composition scheme.

The taxpayer has bills of input tax paid on such goods.

Invoices should not be older than one year from 1st July 2017 (i.e. not dated before 1st July 2016).

Compliance Dashboard

A composition dealer must issue a Bill of Supply and cannot issue a tax invoice

A composition dealer is required to pay tax under Reverse Charge Mechanism (RCM) wherever applicable.

A composition dealer must file quarterly returns using Form CMP-08 and an annual return using Form GSTR-4 under the GST framework.

Composition dealer is not allowed to avail input tax credit of GST on purchases Quarterly payment of taxes

A composition dealer is not allowed to collect composition tax from the buyer

The composition scheme is available only for dealers doing intra-state

Composition scheme is considered to be opted for all businesses that are associated with a PAN. (if one branch is registered under regular having same PAN other branches also disqualify to opt for composition scheme)

Benefits of the composition scheme

Easier and lesser number of compliances to be followed (returns, maintaining books of record, issuance of invoices, etc.)

Quarterly payment of taxes

A limited tax liability

High liquidity as taxes are at a lower rate

Drawbacks of the composition scheme

A limited territory of business, as the dealer is barred from carrying out inter-state transactions

No input tax credit is available to composition dealers

The taxpayer will not be eligible to supply non-taxable goods under GST such as alcohol and goods through an e-commerce portal.